Miami Beach sits on a barrier island where condominiums outnumber single-family homes by roughly ten to one — and every condo appraisal demands building-level analysis that no automated tool performs.

Jhovan F. Rojas, FL Certified Residential Appraiser (License RD6109) at Home Value Inc., authors USPAP-compliant appraisal reports for Miami Beach condos, oceanfront estates, Art Deco district properties, and island residences for lending, divorce, tax protest, PMI removal, and general market value purposes.

Florida’s post-Surfside SB 4-D condo law, FEMA flood zone exposure, and seasonal price cycles make Miami Beach the most appraisal-intensive submarket in Miami-Dade County.

Miami Beach property owners and buyers navigating SB 4-D exposure and seasonal pricing need a certified valuation, not an estimate — book your appraisal with Home Value Inc. at (786) 357-6511.

Appraising a Miami Beach property means evaluating two assets simultaneously: the individual unit or home and the building or environment it occupies.

Jhovan F. Rojas at Home Value Inc. inspects the subject property on-site, measures gross living area, photographs all interior and exterior spaces, and documents the condition details that drive value — floor elevation, view exposure, balcony dimensions, finish level, direct water access, and dock configuration.

The second layer of analysis separates a Miami Beach appraisal from standard residential work.

For condominiums, Rojas reviews the HOA’s financial statements, Structural Integrity Reserve Study (SIRS), milestone inspection report, pending special assessments, and Fannie Mae project eligibility status before selecting comparables or calculating adjustments.

For single-family waterfront estates, the analysis accounts for navigable water access, seawall condition, lot orientation, and FEMA flood zone classification.

Each completed report carries the evidentiary weight required by Florida mortgage lenders, Miami-Dade County Family Court, and federal agencies — the same standard that a Zillow Zestimate, a real estate agent CMA, or a home inspection cannot satisfy.

| What Each Valuation Covers | FL Certified Appraiser | Agent CMA | AVM (Zillow) |

| Written, legally defensible value opinion | Yes | No | No |

| Lender and court acceptance | Yes | No | No |

| HOA reserve and special assessment review | Yes | No | No |

| SB 4-D milestone inspection analysis | Yes | No | No |

| Floor-level and view-quality adjustment | Yes | Rarely | No |

| FEMA flood zone cost impact | Yes | No | No |

Only an FL-certified appraiser delivers a report that satisfies all six criteria above. This distinction matters most in divorce proceedings, probate, and any transaction where opposing parties or regulatory bodies require a credentialed, defensible number.

Four overlapping factors converge on this seven-mile barrier island to create valuation challenges that exist nowhere else in Miami-Dade County.

Condominiums represent the overwhelming majority of Miami Beach’s residential stock. Each unit’s value depends not only on its own condition and location but also on the financial health and structural integrity of the building that houses it.

Two identical floor plans in adjacent towers can carry valuations $100,000 apart based solely on differences in HOA reserve adequacy, pending special assessment exposure, and Condominium Act compliance under Chapter 718, Florida Statutes.

Rojas performs building-level due diligence on every Miami Beach condo assignment — a step that no automated model replicates and that distinguishes a USPAP-compliant appraisal from an estimate.

The Miami Beach Architectural District — spanning much of South Beach and listed on the National Register of Historic Places — subjects properties to Historic Preservation Board review before any exterior alteration proceeds.

Board approval adds 6–12 weeks of project lead time and restricts material choices, paint colors, and structural modifications.

These constraints reduce buyer renovation flexibility and require appraisers to match designated comparables against designated subjects — blending Art Deco and non-designated sales produces unreliable value conclusions.

Home Value Inc. details how preservation rules translate into line-item adjustments in the historic home appraisal challenges guide.

Miami Beach falls almost entirely within FEMA Special Flood Hazard Areas (Zones AE and VE). Flood insurance is mandatory for every federally backed mortgage, and premium variation under FEMA’s Risk Rating 2.0 framework — driven by elevation, proximity to the coast, and construction type — creates net ownership cost differentials that directly affect appraised value.

Rojas factors the impact of flood insurance costs into every Miami Beach report, using the methodology outlined in the Waterfront and Flood Zone Appraisal Guide.

Peak season (November–April) concentrates international and domestic buyer activity on Miami Beach, driving transaction prices 10%–15% above off-season levels in some neighborhoods.

An appraisal conducted in July that relies exclusively on January comparables overstates the current value.

Rojas applies USPAP-required market condition (time) adjustments whenever the effective date and comparable sale dates span different seasonal cycles — a calibration that no AVM performs.

Florida enacted Senate Bill 4-D in May 2022 after the June 2021 Champlain Towers South collapse in Surfside, less than two miles from central Miami Beach. Codified under Florida Statute 553.899, the law created three recurring obligations for every condo and co-op building three stories or taller in Florida:

A Phase 1 milestone structural inspection by a licensed engineer at the 25-year mark for coastal buildings (30 years for others), repeated every 10 years.

A Structural Integrity Reserve Study (SIRS) identifies major building systems, their remaining useful life, and the reserves required to fund replacement. A prohibition on waiving or reducing reserve funding for structural components — effective December 31, 2024.

Miami Beach’s condo stock, built heavily between the 1960s and 1990s, carries disproportionate SB 4-D exposure. Buildings that spent decades minimizing reserve contributions now face catch-up assessments ranging from $30,000 to $175,000 per unit to fund deferred roof replacements, concrete restoration, and waterproofing projects.

Approximately 5,000 Florida condos sit on Fannie Mae’s unavailable list — blocking conventional mortgage financing for every unit in those buildings.

Rojas incorporates three SB 4-D data points into every Miami Beach condo appraisal: the building’s milestone inspection status and findings; the SIRS reserve funding percentage for each structural component; and the dollar amount of current, pending, and anticipated special assessments.

These factors adjust the final value conclusion at the building level — a layer of analysis that sits entirely outside the scope of a CMA, an AVM, or a home inspection.

| Building Age Band | Typical SB 4-D Exposure in Miami Beach |

| Pre-1980 (45+ years) | Milestone inspection completed or overdue; Phase 2 repairs common; highest assessment exposure |

| 1980–1995 (30–45 years) | Milestone inspection triggered or imminent; reserve catch-up underway; moderate-to-high assessment risk |

| 1996–2005 (20–30 years) | Approaching milestone threshold; SIRS required; lower immediate exposure but reserve gaps emerging |

| Post-2005 (under 20 years) | Below milestone trigger: SIRS required within the first year of non-developer ownership; lowest exposure |

The cost of skipping this analysis is measurable. A buyer who closes on a Miami Beach condo without reviewing the SIRS and milestone report can inherit a five- or six-figure assessment levied weeks after closing — a liability that a certified appraisal identifies before the purchase contract is signed.

Understand your Miami Beach condo’s true exposure before you buy, sell, or refinance — talk to Home Value Inc. at (786) 357-6511.

Miami Beach stretches seven miles from South Pointe Park to 87th Terrace, and each corridor follows its own pricing logic. Rojas selects comparables from within the relevant neighborhood rather than blending sales across corridors that serve different buyer profiles and follow independent price trajectories.

| Neighborhood | What Defines It | What the Appraiser Watches |

| South Beach / South of Fifth | Art Deco boutique condos; ultra-luxury SoFi towers; walk-score premiums | Historic district designation, seasonal tourist-driven demand, and short-term rental regulation compliance |

| Mid-Beach (23rd–63rd St) | Faena District; branded oceanfront towers; newer luxury construction | SB 4-D exposure in pre-2000 buildings; floor-level ocean view premiums; HOA fee trajectory |

| North Beach (63rd–87th Terr) | Mid-rise condos; larger lots; year-round owner-occupant base | Renovation-adjusted value in aging stock; lower seasonal volatility; school zone differentials |

| Venetian Islands / Belle Isle | Bay-front single-family estates; limited annual transaction volume | Fewer than 40 closed sales per year combined; waterfront paired-sale analysis required |

| La Gorce Island | Gated ultra-luxury waterfront single-family | Extremely limited data set; direct water access and dock premiums; lot-size dominance in value |

| Normandy Isles / Normandy Shores | Single-family and townhome mix; golf course adjacency | Canal-front premiums; Normandy Shores Golf Club proximity factor; renovation scope flexibility |

| Surfside (adjacent) | Mid-rise and high-rise condos; residential SFR pockets | Post-Champlain Towers buyer sensitivity; SB 4-D compliance scrutiny at peak intensity |

The countywide picture and how Miami Beach fits within it are covered on the Miami real estate appraiser page, and current pricing trends across all Miami-Dade submarkets appear in the 2025 market trend analysis.

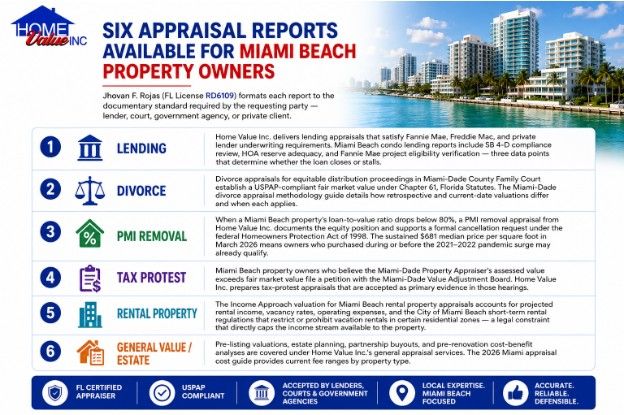

Jhovan F. Rojas (FL License RD6109) formats each report to the documentary standard required by the requesting party — lender, court, government agency, or private client.

Lending — Home Value Inc. delivers lending appraisals that satisfy Fannie Mae, Freddie Mac, and private lender underwriting requirements. Miami Beach condo lending reports include SB 4-D compliance review, HOA reserve adequacy, and Fannie Mae project eligibility verification — three data points that determine whether the loan closes or stalls.

Divorce — Divorce appraisals for equitable distribution proceedings in Miami-Dade County Family Court establish a USPAP-compliant fair market value under Chapter 61, Florida Statutes. The Miami-Dade divorce appraisal methodology guide details how retrospective and current-date valuations differ and when each applies.

PMI Removal — When a Miami Beach property’s loan-to-value ratio drops below 80%, a PMI removal appraisal from Home Value Inc. documents the equity position and supports a formal cancellation request under the federal Homeowners Protection Act of 1998. The sustained $681 median price per square foot in March 2026 means owners who purchased during or before the 2021–2022 pandemic surge may already qualify.

Tax Protest — Miami Beach property owners who believe the Miami-Dade Property Appraiser’s assessed value exceeds fair market value file a petition with the Miami-Dade Value Adjustment Board. Home Value Inc. prepares tax-protest appraisals that are accepted as primary evidence in those hearings.

Rental Property — The Income Approach valuation for Miami Beach rental property appraisals accounts for projected rental income, vacancy rates, operating expenses, and the City of Miami Beach short-term rental regulations that restrict or prohibit vacation rentals in certain residential zones — a legal constraint that directly caps the income stream available to the property.

General Value / Estate — Pre-listing valuations, estate planning, partnership buyouts, and pre-renovation cost-benefit analyses are covered under Home Value Inc.’s general appraisal services. The 2026 Miami appraisal cost guide provides current fee ranges by property type.

Home Value Inc. moves every Miami Beach assignment through four stages — consultation, inspection, analysis, and delivery — with a turnaround of 3–5 business days under standard scheduling and same-day delivery available on qualifying residential assignments.

Consultation — A property owner, attorney, or lender calls (786) 357-6511 to open an assignment. Rojas confirms the property type, appraisal purpose, delivery timeline, and — for condos — the building’s SB 4-D compliance status and any pending assessments. This step is free and confidential.

Inspection — Rojas visits the Miami Beach property and spends one to two hours on site. Condo inspections document the finish level, floor elevation, view quality, balcony dimensions, and access to building amenities. Single-family and waterfront inspections cover structure, lot characteristics, seawall condition, dock rights, and FEMA flood zone classification.

Analysis — Rojas pulls qualified comparable sales from within the relevant Miami Beach neighborhood using MLS records and Miami-Dade County public property data. Adjustments address gross living area, floor level, view exposure, waterfront access, building age, HOA fees, SB 4-D status, and seasonal market timing.

The property valuation guide published by Home Value Inc. explains the three USPAP-recognized approaches — Sales Comparison, Income, and Cost — and when each applies. For details on factors that extend the timeline on complex assignments, the appraisal turnaround guide covers the full picture.

Delivery — The completed USPAP-compliant report goes to the lender portal on lending assignments and to the retaining attorney or client in PDF format on divorce, estate, and tax protest work.

Home Value Inc. operates from 383 Westward Dr, Miami Springs, FL 33166 and has appraised properties across every Miami Beach corridor — South Beach, Mid-Beach, North Beach, the Venetian Islands, La Gorce Island, Normandy Isles, and Surfside.

Jhovan F. Rojas holds an FL Certified Residential Appraiser License RD6109, verified through the DBPR, and maintains a proprietary property database covering the full Miami-Dade County market. Free consultations are available by phone at (786) 357-6511.

What does a Miami Beach condo appraisal cost in 2026?

Standard condo appraisals in Miami Beach range from $450 to $800 depending on unit size, building complexity, and turnaround requirements. Oceanfront towers, luxury penthouses, and multi-family assignments typically run $800 to $1,500 or more. Call (786) 357-6511 for assignment-specific pricing.

How quickly can Home Value Inc. deliver a Miami Beach appraisal report?

Standard delivery runs 3–5 business days from the on-site inspection. Same-day written reports are available on qualifying residential assignments. The inspection itself takes one to two hours on site, depending on unit size, building access, and whether waterfront or condo-specific documentation review is required.

What documents should I gather before my Miami Beach condo appraisal?

Gather the building’s most recent SIRS, milestone inspection report if available, two years of HOA financial statements, and records of any pending or recently levied special assessments. Compiling permitted improvement receipts and contractor invoices from the past five years helps the appraiser calculate accurate condition adjustments.

How does SB 4-D change my Miami Beach condo’s appraised value?

SB 4-D forces older buildings to fund deferred structural maintenance through special assessments that reduce net unit value dollar-for-dollar. Rojas reviews the building’s milestone inspection findings, SIRS reserve levels, and assessment exposure on every condo assignment to capture building-level financial risk in the final valuation.

Can I use a Miami Beach appraisal to cancel my private mortgage insurance?

Homeowners whose Miami Beach property has appreciated past the 80% loan-to-value threshold submit a USPAP-compliant appraisal from Home Value Inc. to their mortgage servicer with a formal PMI cancellation request under the federal Homeowners Protection Act.

Does Home Value Inc. handle divorce appraisals for Miami Beach real estate?

Rojas delivers USPAP-compliant divorce appraisals for equitable distribution proceedings in Miami-Dade County Family Court. Each report meets the evidentiary standard for marital asset division under Chapter 61, Florida Statutes, including retrospective valuations tied to a specific separation date when required.

Why do seasonal price swings matter in a Miami Beach appraisal?

Peak-season sales (November–April) trade at measurably higher prices than off-season closings in the same building. Rojas applies USPAP-required market condition adjustments to comparables when sale dates and the effective appraisal date fall in different seasonal cycles, preventing inflated or deflated conclusions.

What is the Fannie Mae unavailable list, and how does it affect my condo?

Condo buildings that fail to meet Fannie Mae’s insurance, reserve, or structural compliance standards land on the unavailable list, blocking conventional mortgage financing for every unit in the building. Rojas verifies Fannie Mae eligibility during scope confirmation so clients understand financing limitations before committing.

How do waterfront premiums get calculated on Miami Beach island properties?

Rojas quantifies waterfront premiums through recent paired sales — matching waterfront closings against comparable non-waterfront sales in the same neighborhood — rather than applying rule-of-thumb percentage adjustments. Direct water access, dock rights, seawall condition, and lot orientation each receive separate line-item treatment.

Which parts of Miami Beach does Home Value Inc. cover?

Home Value Inc. covers all of Miami Beach — South Beach, South of Fifth, Mid-Beach, North Beach, Sunset Harbor, the Venetian Islands, Belle Isle, La Gorce Island, Normandy Isles, Normandy Shores, and adjacent Surfside. Rojas draws comparables from the specific corridor, never the broader island.

An algorithm cannot read your building’s reserve study, verify your milestone inspection, or adjust for the floor you live on — get a certified Miami Beach appraisal from Home Value Inc. at (786) 357-6511.

Home Value Inc. performs residential and commercial appraisals for its clients in greater Miami-Dade County and the following cities in South Florida. We provide services to the following cities -