A Reconsideration of Value (ROV) is an evidence-based request a mortgage borrower submits to a lender asking the original appraiser to review specific factual corrections or omitted market data that could affect the appraised value.

An ROV is not an appeal, and an ROV is not a complaint. An ROV is a structured submission that identifies a measurable deficiency, such as an incorrect gross living area, an incorrect bedroom count, or a missed closed comparable sale, and then asks whether the new evidence changes the value conclusion.

Miami-Dade borrowers who want a second, independent value opinion to support negotiation can start with a general value appraisal before deciding whether an ROV package is worth submitting.

Borrowers should treat an ROV as a time-sensitive underwriting workflow rather than a negotiation tactic. Most lender processes allow a borrower to submit only one borrower-initiated ROV per appraisal, making evidence quality and completeness the deciding factor in outcomes.

A borrower must submit an ROV early enough for the lender, the appraisal management company, and the appraiser to complete review before the scheduled closing date.

Borrowers who want a faster timeline should review the common causes of appraisal delays and avoid submission mistakes that trigger resubmission loops.

Florida mortgage borrowers interact with ROV requirements through overlapping frameworks.

The frameworks include GSE requirements, interagency guidance, and loan-program policies enforced by the lender or appraisal management company.

ROV outcomes depend on whether the submission corrects a report fact or supplies better market support than the original comparable selection.

Borrowers who want the appraisal methodology context should review the South Florida process before selecting comparables or disputing adjustments.

If you’re ready to get started, call us now!

The appraisal report lists the appraiser, the appraisal effective date, the comparable sales, and the adjustments. A borrower should verify addresses, sale dates, sale prices, gross living area figures, bedroom and bath counts, and condition descriptions before drafting the ROV narrative.

Borrowers who need a quick framework for what appraisers document in a standard inspection can cross-check against a home appraisal checklist to spot missing items that could become factual corrections.

A valid ROV identifies an error that the appraiser can verify. A valid ROV example includes an incorrect square footage figure contradicted by county records, a missed closed comparable sale, or a feature documented as absent when the feature exists and can be photographed.

A borrower should avoid framing the submission as “the value is too low.” A value disagreement without a factual deficiency gives the lender no compliant basis to forward the package for review.

A strong ROV uses closed transactions, not listings or pending sales. A borrower should choose comparable sales that closed on or before the appraisal effective date, then attach MLS sheets or equivalent third-party evidence that shows sale price, sale date, living area, bed and bath count, and address.

Borrowers in micro-markets with thin data, such as waterfront corridors, should confirm how scarce comps affect selection by reviewing waterfront appraisals before submitting weak or non-comparable sales.

A compliant ROV package states the deficiency and attaches evidence. A compliant ROV package does not request a specific dollar outcome and does not include the value needed to close. Lenders screen for value pressure because appraisal independence rules prohibit coercion or influence over the appraiser’s opinion of value.

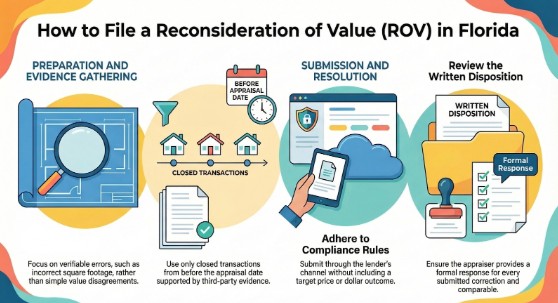

A borrower routes the ROV through the lender’s defined channel so the lender can log the request, screen for completeness, and forward the package to the appraiser or appraisal management company.

Borrowers preparing documentation should follow a pre-appraisal checklist so photos, improvement lists, and access details do not become preventable friction points.

A compliant ROV outcome includes a written disposition for each submitted comparable sale and each factual correction. The appraiser either revises the report and value conclusion or explains why the evidence does not support a change. The lender communicates the result to the borrower.

A borrower who receives a no-change response should pivot to a decision that affects closing. The borrower can renegotiate the price, increase the down payment, or ask the lender whether a second appraisal is warranted due to a material deficiency.

Borrowers who plan to refinance rather than close the current transaction should understand how a new valuation enters underwriting by reviewing mortgage refinancing appraisal workflows.

If you’re ready to get started, call us now!

A successful Florida ROV package uses verifiable data that maps to an appraisal adjustment or a report fact statement.

Borrowers who want a plain-English explanation of what value evidence matters most can start with property appraisal benefits to align effort with decision impact.

Florida lenders and AMCs reject ROV submissions that violate independence rules or fail closed-sale requirements.

Borrowers who want a reality check on automated value ranges versus certified reports should review online appraisal accuracy before relying on algorithm estimates in an ROV package.

A low appraisal in Miami-Dade County often reflects a data mismatch rather than a final verdict. A borrower increases ROV success by submitting closed comparable sales, documented factual corrections, and evidence tied to appraisal adjustments.

Home Value Inc performs certified residential and commercial appraisals throughout Miami-Dade County.

Jhovan F. Rojas, Florida Certified Residential Appraiser (License No. RD6109), has appraised properties in South Florida since 2006.

A low appraisal creates five realistic options. A borrower can submit an ROV with factual corrections, ask whether the lender will order a second appraisal for a material deficiency, order an independent appraisal for negotiation support, renegotiate the price, or exit under an appraisal contingency.

A Reconsideration of Value is a borrower-initiated, evidence-based request submitted to a lender asking the original appraiser to review specific factual corrections or missed closed comparable sales. The lender controls the workflow to ensure the submission remains compliant with appraiser independence requirements.

ROV timelines vary by lender, AMC, and closing date. Many lenders respond within 5 to 10 business days, but the practical constraint is closing. Borrowers should initiate an ROV within 24 to 48 hours after receiving the appraisal report.

Borrowers who want clearer timeline expectations should compare lender timing against the typical appraisal timeline for Miami-Dade assignments.

A borrower should route value reconsideration through the lender or appraisal management company, not through direct contact with the appraiser. Lender-managed communication reduces the risk of coercion and supports fair lending safeguards.

Most conventional loan workflows treat one borrower-initiated ROV as the practical limit, so the borrower should submit one complete, evidence-based package. If the value does not change, the next options are renegotiation, a larger down payment, or lender discretion for a second appraisal.

A Florida ROV explanation should list one factual deficiency per bullet, cite supporting documents, and reference closed comparable sales that the report did not use. A Florida ROV explanation should not state a target value, a value range, or the dollar amount needed to close.

A borrower should start an ROV within 24 to 48 hours of receiving the appraisal report by reading the comps, verifying property facts, and assembling closed-sale evidence. A borrower should submit one complete package through the lender’s defined channel to avoid resubmissions.

About the Author

South Florida Residential Appraiser · Expert Witness · Residential Valuation Specialist

Jhovan Rojas is a South Florida residential real estate appraiser with more than 20 years of experience valuing residential properties throughout Miami-Dade, Broward, and Palm Beach Counties. His appraisal experience spans multiple real estate market cycles, including the foreclosure-driven downturn of the late 2000s, the subsequent recovery period, and the rapid appreciation that followed the COVID-19 housing boom.

Throughout his career, Jhovan has appraised thousands of residential properties, including single-family homes, condominiums, multi-family residences, luxury estates, waterfront properties with boating access, and complex high-value residential assets. His expertise includes residential valuation, appraisal review, market analysis, lender compliance review, and expert witness services for litigation involving real estate valuation disputes.

In addition to performing residential appraisals, Jhovan has conducted appraisal reviews for lending institutions, supervised and mentored trainee appraisers, and provided expert testimony in divorce and property-related legal matters. He is also a frequent speaker for Realtor and broker education programs, where he shares insights on valuation methodology, appraisal standards, market trends, and factors influencing residential property values throughout South Florida.

Drawing on decades of hands-on appraisal experience, Jhovan helps homeowners, attorneys, lenders, real estate professionals, and property investors make informed decisions based on credible, well-supported valuation analysis.

Home Value Inc. performs residential and commercial appraisals for its clients in greater Miami-Dade County and the following cities in South Florida. We provide services to the following cities -