Home Value Inc. is a licensed real estate appraiser serving Homestead and South Miami-Dade, Florida, delivering Florida State Certified, USPAP-compliant valuations across the county’s most geographically and environmentally complex submarket — agricultural parcels in the Redlands district, flood-zone residential properties with FEMA 50% Rule exposure, pre-1992 housing stock subject to post-Andrew building code bifurcation, and value-tier single-family homes in Florida City, Leisure City, and Princeton.

Homestead property owners scheduling a lending appraisal receive a certified report with FEMA flood zone analysis and storm-history condition adjustments built into every residential assignment — typically within 2–3 business days.

Homestead and South Miami-Dade owners requiring a property tax protest, estate settlement, agricultural land valuation, or FEMA 50% Rule pre-improvement appraisal receive the same USPAP-compliant standard, with report timelines confirmed at scope based on property type and complexity.

Schedule your Homestead or South Miami-Dade appraisal with Home Value Inc. Contact Home Value Inc. to confirm assignment scope and inspection availability.

Home Value Inc. appraisers operating in Homestead and South Miami-Dade resolve valuation challenges that do not exist in any other submarket in this geo page series — FEMA 50% Rule pre-improvement valuations that determine whether a renovation triggers full floodplain compliance.

Hurricane Andrew building code bifurcation adjustments that separate pre-1992 from post-1992 construction value, and agricultural land income capitalization that requires crop production data, soil classification, and irrigation infrastructure analysis rather than comparable sales.

The Florida Department of Business and Professional Regulation licenses and governs every Florida State Certified appraiser — the credential standard every Home Value Inc. appraisal report carries, regardless of property type or assignment complexity.

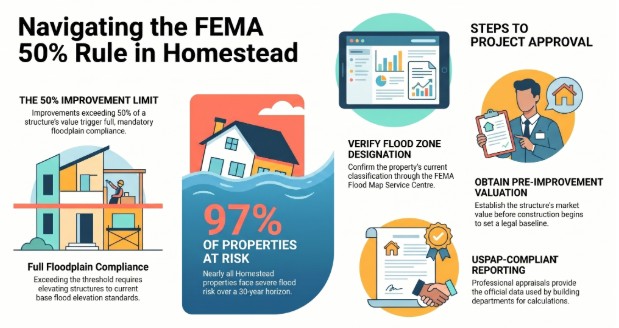

The FEMA 50% Rule prohibits improvements to a structure in a Special Flood Hazard Area that exceed 50% of the structure’s pre-improvement market value without triggering full floodplain compliance — including elevation to current base flood elevation standards under the National Flood Insurance Program.

In Homestead, where First Street Foundation data show that 97% of properties face severe flood risk over a 30-year horizon, this rule creates an appraisal assignment category that other Miami-Dade submarkets rarely require: the pre-improvement retrospective valuation.

Homestead property owners planning renovations, additions, or storm damage repairs must establish the structure’s pre-improvement market value before construction begins — so the local building department can determine whether the planned work triggers the 50% threshold.

Home Value Inc. appraisers complete FEMA 50% Rule pre-improvement valuations for Homestead residential and agricultural structures, producing a USPAP-compliant written report that establishes the baseline value the building department uses for the substantial improvement calculation.

Homeowners can verify their property’s current FEMA Flood Insurance Rate Map zone designation through the FEMA Flood Map Service Center before scheduling an appraisal, so the assignment scope reflects the correct flood zone classification from the outset.

If you’re ready to get started, call us now!

Hurricane Andrew made Category 5 landfall near Homestead on August 24, 1992, with sustained winds of 165 mph and gusts to 177 mph — destroying more than 99% of mobile homes in the city and triggering the Florida Building Code reforms that now govern all residential construction in the state.

Homestead’s housing stock splits into two construction vintage categories that require different condition and quality adjustments in every comparable analysis.

Pre-1992 construction in Homestead often lacks the reinforced roof structures, impact-resistant windows, and elevated foundations that the post-Andrew Florida Building Code requires — physical deficiencies that reduce effective age, increase insurance costs, and require explicit condition adjustments when pre-1992 homes are used as comparables for post-1992 subject properties.

Post-1992 construction built to updated code standards commands a measurable premium over pre-1992 stock of equivalent size and location — a premium Home Value Inc. appraisers quantify through matched-pair analysis rather than applying a generic age adjustment.

The property appraisal process in South Florida covers the full condition and quality adjustment methodology Home Value Inc. applies to complex construction-vintage assignments.

Agricultural land in the Redlands district of South Miami-Dade requires income capitalization methodology rather than the sales comparison approach used for residential assignments — so buyers, lenders, and estate planners receive a value grounded in the land’s actual productive capacity rather than a price-per-acre metric derived from dissimilar parcels.

Southern Miami-Dade’s Redlands district is home to Florida’s largest greenhouse and nursery industry, with active avocado groves, tropical fruit farms, and ornamental plant operations that trade on soil classification, irrigation infrastructure, and crop income data.

Home Value Inc. appraisers derive agricultural land value from verified crop income, soil productivity classification, irrigation system condition, and market-derived capitalization rates specific to South Miami-Dade’s agricultural submarket — then reconcile the income approach with available comparable land sales adjusted for soil quality and water access.

Canal-front agricultural parcels in the Redlands command premiums over non-irrigated parcels, requiring explicit matched-pair analysis to quantify them accurately.

The Miami-Dade appraisal process covers the comparable selection and income methodology framework that Home Value Inc. applies across all South Florida property types.

Home Value Inc. completes agricultural, flood-zone, and residential appraisals across all Homestead and South Miami-Dade communities. Contact Home Value Inc. to confirm your assignment type and inspection timeline.

If you’re ready to get started, call us now!

Lending appraisals for Homestead purchase transactions and mortgage refinancing require FEMA flood zone verification, construction vintage identification, and — on pre-1992 properties — explicit building code condition adjustments — so lenders receive a value that reflects the subject property’s actual insurability and structural compliance status under current Florida Building Code standards.

Divorce appraisals in Miami-Dade for Homestead properties require court-defensible methodology and, where necessary, retrospective valuations tied to a specific date of separation — so attorneys and their clients receive a value opinion that accounts for the subject property’s flood zone designation, construction vintage, and storm damage history as of the effective date.

General value appraisals structured for FEMA 50% Rule compliance establish the pre-improvement market value of a Homestead structure before renovation or repair work begins — so property owners can determine whether planned work triggers full floodplain compliance requirements before construction contracts are signed.

Property tax protest appraisals provide the independent valuation evidence Homestead property owners need to challenge an inflated Miami-Dade County assessment before the Miami-Dade Value Adjustment Board — so you can reduce your annual tax liability with a certified appraisal that reflects Homestead’s value-tier pricing rather than county-wide benchmarks.

The Florida reconsideration process covers every step for owners who believe a completed appraisal does not reflect current South Miami-Dade market conditions.

Estate and probate appraisals establish date-of-death values for Homestead and South Miami-Dade properties moving through Florida probate — so executors and attorneys can satisfy court documentation requirements with a certified, USPAP-compliant report that reflects the subject property’s flood zone classification, construction vintage, and agricultural use status where applicable.

PMI removal appraisals establish current market value for Homestead homeowners who have reached 20% equity in their property, so you can eliminate the monthly private mortgage insurance cost through an independent lender-accepted valuation supported by Homestead-specific comparable sales at the value-tier pricing level.

Home Value Inc. structures every Homestead appraisal around the assignment’s specific complexity — FEMA flood zone status, construction vintage, and property type each determine which methodology and documentation standards apply before the inspection is scheduled.

Home Value Inc. confirms FEMA Flood Insurance Rate Map zone designation, construction vintage relative to the August 24, 1992, Andrew landfall date, property type, intended use, and the identity of all intended users before scheduling the inspection — so the correct methodology is selected and the field work produces the specific data each assignment requires.

FEMA 50% Rule assignments require the appraiser to document the structure’s pre-improvement condition as of the inspection date, making early scope confirmation essential to avoid inspection timing conflicts with planned construction.

The appraiser conducts an on-site inspection, documenting flood zone exposure indicators, construction vintage markers, storm-damage repair history, permitted improvement records, and — on agricultural parcels — irrigation infrastructure condition, soil classification documentation, and crop operation status.

Pre-1992 residential inspections specifically document roof structure type, window impact resistance, and foundation elevation relative to current base flood elevation, because these elements drive the condition and quality adjustments that separate pre- and post-Andrew comparable sales.

The appraisal preparation guide details every document to have ready before the appraiser arrives.

Homestead single-family residential assignments use the sales comparison approach with value-tier comparable selection — drawing from Homestead, Florida City, Leisure City, and Princeton rather than the broader Miami-Dade medians, which overstate local market value by more than 30%.

Agricultural assignments use the income capitalization approach derived from verified crop income and soil productivity data. FEMA 50% Rule assignments use the sales comparison and cost approaches to establish pre-improvement market value as of the inspection date.

USPAP Standards Rule 1-6 governs value reconciliation on every assignment — the standard Home Value Inc. applies across all Homestead property types.

Homestead property owners who assemble the right documentation before the inspection give the appraiser the evidence needed to support flood zone adjustments, construction vintage determinations, and storm damage condition assessments in the final report — so the value reflects actual property characteristics rather than assessor record assumptions.

Home Value Inc. recommends that Homestead residential owners confirm their FEMA Flood Insurance Rate Map zone through the FEMA Flood Map Service Center and gather any elevation certificate previously issued for the property, so the appraiser can address base flood elevation compliance and insurance cost impact in the report.

Property owners planning renovations should compile contractor bids and scope-of-work documents before the inspection, so the pre-improvement value can be established before construction begins, rather than being reconstructed retrospectively.

Agricultural landowners should compile the prior two years of crop income records and any soil productivity reports, so the appraiser has verified production data to support the income capitalization analysis.

Homeowners can verify current assessment data and permit history using the Miami-Dade County Property Appraiser’s public records database before the inspection date. The 2025 appraisal checklist covers every document organized by property type.

Home Value Inc. serves all Homestead and South Miami-Dade communities. Contact Home Value Inc. to schedule your appraisal and confirm flood zone, agricultural, or FEMA 50% Rule assignment requirements.

How much does a real estate appraisal cost in Homestead or South Miami-Dade?

A standard residential appraisal in Homestead costs between $400 and $650 as of 2026. Agricultural land, FEMA 50% Rule pre-improvement, and complex flood-zone assignments range from $650 to $1,200 or more, depending on acreage, crop documentation requirements, and report complexity.

What is the FEMA 50% Rule, and why does it require a certified appraisal in Homestead?

The FEMA 50% Rule prohibits improvements to a Special Flood Hazard Area structure that exceed 50% of the pre-improvement market value without triggering full floodplain compliance. In Homestead, where 97% of properties face severe flood risk, a certified pre-improvement appraisal from Home Value Inc. establishes the baseline value the building department uses for the threshold calculation.

How does Hurricane Andrew’s 1992 landfall affect Homestead property appraisals today?

Hurricane Andrew triggered Florida Building Code reforms that created a permanent condition and quality divide between pre-1992 and post-1992 Homestead construction. Home Value Inc. appraisers identify construction vintage on every Homestead assignment and apply matched-pair adjustments to quantify the premium post-Andrew code-compliant construction commands over pre-1992 stock.

How does Home Value Inc. appraise agricultural land in Redlands?

Home Value Inc. appraises Redlands agricultural parcels using the income capitalization methodology — deriving value from verified crop income, soil productivity classification, and irrigation infrastructure condition, then capitalizing net agricultural income at a market-derived rate specific to South Miami-Dade’s agricultural submarket as of the effective date.

Does Home Value Inc. provide retrospective appraisals for Homestead properties?

Yes. Home Value Inc. provides retrospective appraisals establishing property value as of a past effective date — required for divorce proceedings, estate settlement, capital gains calculations, and FEMA 50% Rule pre-storm baseline determinations. The divorce appraisal methodology page details documentation standards for every retrospective Homestead assignment.

What is a USPAP-compliant appraisal, and why does it matter in Homestead?

A USPAP-compliant appraisal follows the Uniform Standards of Professional Appraisal Practice — the federally recognized performance standards governing all licensed appraisers in the United States. USPAP compliance is required for appraisals used in mortgage lending, FEMA 50% Rule determinations, estate settlements, divorce proceedings, and property tax appeals before the Miami-Dade Value Adjustment Board.

Which Homestead and South Miami-Dade communities does Home Value Inc. serve?

Home Value Inc. appraises properties across all Homestead and South Miami-Dade communities — Homestead city limits, Florida City, Leisure City, Princeton, the Redlands agricultural district, Naranja, and the South Dade corridor to the Florida Keys approach. For properties in neighboring Biscayne Park, the Biscayne Park appraiser page covers that submarket.

About the Author

South Florida Residential Appraiser · Expert Witness · Residential Valuation Specialist

Jhovan Rojas is a South Florida residential real estate appraiser with more than 20 years of experience valuing residential properties throughout Miami-Dade, Broward, and Palm Beach Counties. His appraisal experience spans multiple real estate market cycles, including the foreclosure-driven downturn of the late 2000s, the subsequent recovery period, and the rapid appreciation that followed the COVID-19 housing boom.

Throughout his career, Jhovan has appraised thousands of residential properties, including single-family homes, condominiums, multi-family residences, luxury estates, waterfront properties with boating access, and complex high-value residential assets. His expertise includes residential valuation, appraisal review, market analysis, lender compliance review, and expert witness services for litigation involving real estate valuation disputes.

In addition to performing residential appraisals, Jhovan has conducted appraisal reviews for lending institutions, supervised and mentored trainee appraisers, and provided expert testimony in divorce and property-related legal matters. He is also a frequent speaker for Realtor and broker education programs, where he shares insights on valuation methodology, appraisal standards, market trends, and factors influencing residential property values throughout South Florida.

Drawing on decades of hands-on appraisal experience, Jhovan helps homeowners, attorneys, lenders, real estate professionals, and property investors make informed decisions based on credible, well-supported valuation analysis.

Home Value Inc. performs residential and commercial appraisals for its clients in greater Miami-Dade County and the following cities in South Florida. We provide services to the following cities -